UAE walks out, Fed decision & Big tech earnings

- Global markets kick off Wednesday mixed

- 5 of "Mag 7" expected to report results this week

- UAE exits OPEC, Oil prices supported by Iran war

- Fed expected to leave rates unchanged

Equity markets kicked off Wednesday on a shaky note with Asian shares mixed amid geopolitical risk and concerns over the health of the AI sector.

An impasse between the United States and Iran continues to drain risk sentiment, with market fatigue building due to the back and forth. This uncertainty may cap equity markets ahead of the Fed decision and earnings from tech titans.

Speaking of tech, AI payback concerns returned like an itch after the Wall Street Journal reported that OpenAI missed internal targets. Despite OpenAI pushing back, investors may start questioning whether the massive AI spending will pay off. A projected $600billion of capital spending expected between Alphabet, Amazon, Meta Platforms and Microsoft this year.

Five of the so-called “Magnificent” 7 tech giants with a combined market cap of almost $16 trillion are set to publish their results over the next two days.

Considering how the combined weight of Alphabet, Amazon, Meta, Microsoft and Apple make up over 40% of the Nasdaq 100 weight, this could mean extreme levels of volatility.

The Federal Reserve is widely expected to leave interest rates unchanged when it meets this evening.

But the more interesting topic will be whether Powell stays on at the Fed or leaves after his term expires in mid-May. With Iran-US peace talks in limbo, the Strait of Hormuz closed and oil prices elevated -the Fed is likely to move ahead with a hawkish hold.

Traders are currently pricing a less than 20% chance that the Fed cuts rates by the end of 2026.

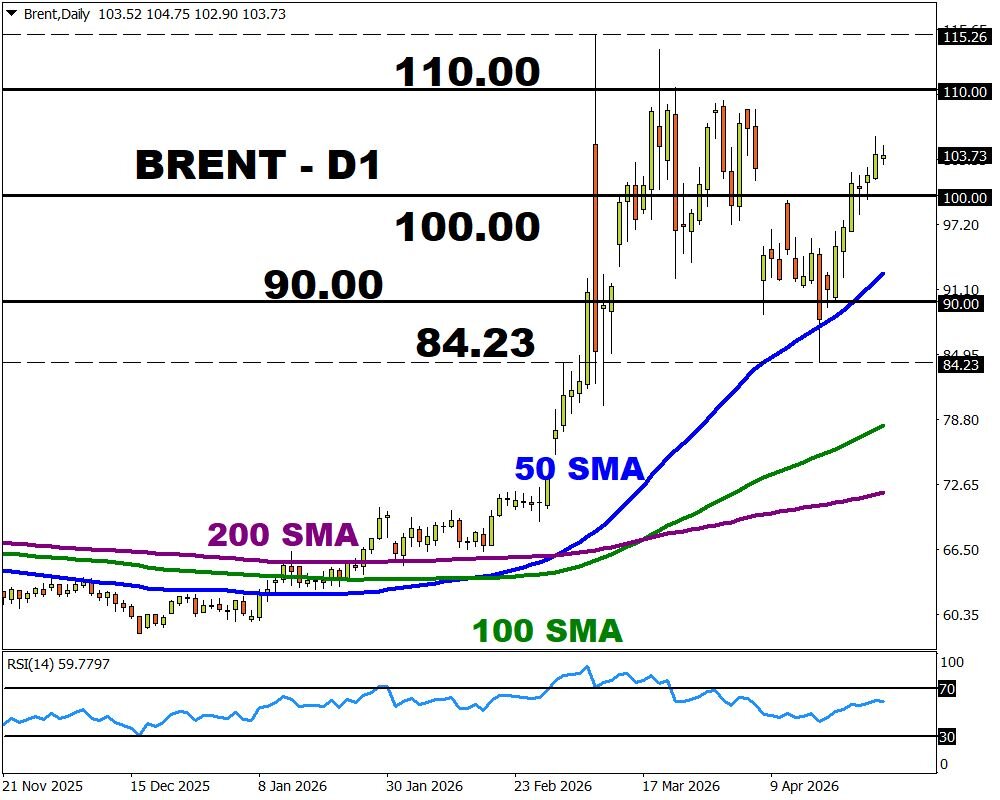

In the commodity space, the UAE exit is a major blow to OPEC and something that may reshape the dynamics in the global energy markets.

Given how the Strait of Hormuz remains closed, the UAE’s exit will have a limited impact on oil markets for now.

However, the longer-term implications are bearish for oil given a weaker OPEC internally.

Should other members start to leave the cartel and pump without production limits, the prospect of increased supply in the longer term may spell weaker oil prices.

In the meantime, Brent remains at triple-digits as traders await Washington’s response to a proposal from Tehran to end the war.